Economic Justice for All New Yorkers

News & Events

Groups, Tenants, Electeds Rally at City Hall, Demand Council Boost Community Land Trusts To Keep New Yorkers Housed

On Thursday, more than 50 community, housing, and environmental justice groups and elected officials rallied at City Hall for the Community...[more]

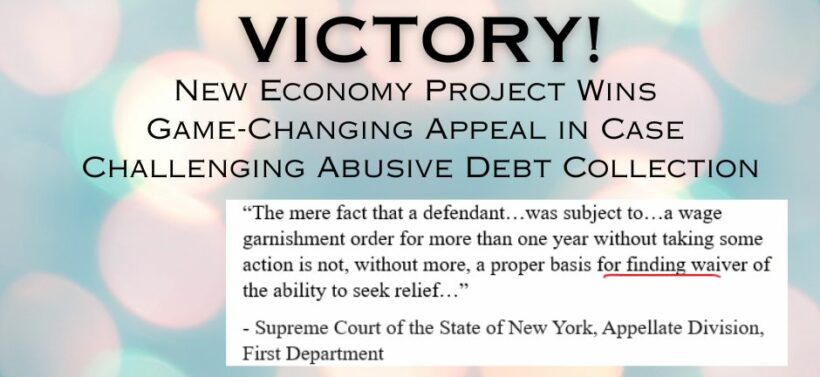

The City: Pushback Grows as Council and Mayor Hash Out Deal to Revive Property Debt Sell-Off

The City -- With Mayor Eric Adams’ administration and the City Council in talks to revive a controversial property tax-collection...[more]

New York Law Journal – Commentary: Give New Yorkers a Consumer Protection Law They Can Actually Use

New York should pass the Consumer and Small business Protection Act as an urgent matter of racial and economic justice,...[more]